Employing capital to radically retool an infrastructure has a case study:

Nothing Like It in the World by Stephen Ambrose, how the Transcontinental Railroads were built. Private construction capital (risk on the innovators) reinforced by government-backed bonds once networks were in operation and achieving public policy objectives.

Four Types of Companies:

As with building the Internet and Transcontinental Railroads, companies must be created to be single-purpose. There may be overlapping of similar shareholders, but each type of company will have independent ownership, management, and operations:

- Capital: JPods Capital LLC and similar companies provide capital and enforced fiscal discipline.

- Technology: JPods LLC. JPods profits by creating and enforcing technology standards that are desired by the farebox payer.

- Construction: Master Mobility Companies® (MMCs) are licensed to build JPods networks within specific legal jurisdictions. They are the experts in building under the laws of that jurisdiction. MMCs profit by building networks and selling them to Local Mobility Companies.

- Operations: Local Mobility Companies® (LMCs) are licensed to own and operate networks within a specific economic community. MMCs profit from the fare box, moving cargo and people.

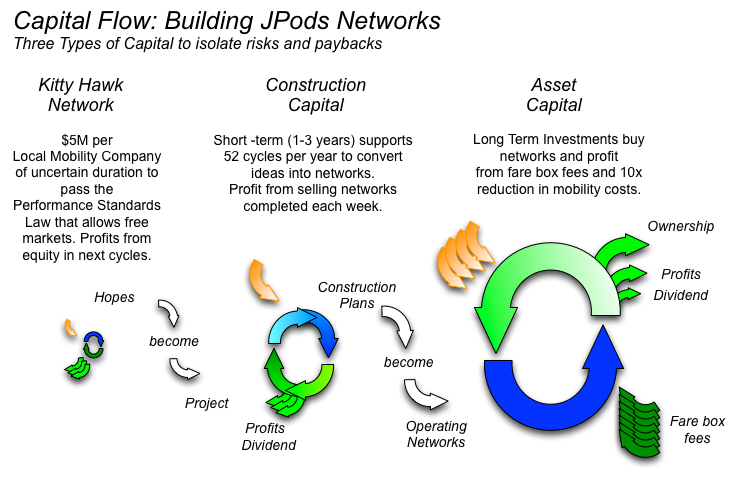

Three Types of Capital:

Three different types of capital are employed by Local Mobility and Master Mobility Companies. An explanation is provided below to understand the cycles in the graphic.

- Kitty Hawk Networks™ Capital supports the startup phase of LMCs (Local Mobility Companies own and operate the networks):

- LMCs are the ISPs of the Physical Internet®. They are the retailer aspect of transportation.

- Rights of Way access is THE pacing item and must have the 5X5% Performance Standard.

- LMCs should risk very little until the 5X5% Performance Standard is adopted by the local governments:

- Networks must be constructed with private funds.

- Networks must operate without government subsidies.

- 5X – Networks 5 times more efficient than existing government networks are approved to build unless governments write a written rejection. This shift the nature of bureaucracies to do nothing in favor of sustainable innovations.

- 5% – Networks must pay 5% of gross revenues for non-exclusive use of RIghts of Way.

- Networks are regulated by the ASTM F24 standards used in a state to regulate theme park thrill rides:

- Radically better safety record:

- ASTM: 0.2 injuries per million

- DOT: 11,200 injuries per million

- Existing regulations, no delay while bureaucracies write new regulations.

- Existing enforcement

- Existing common law

- Radically better safety record:

- Process and support documentation to implement the 5X5% Performance Standard.

- PathFinder agreement for local people to form Local Mobility Companies in their cities. This will shift over time to gamify getting opportunities for people to participate in creating LMCs.

- The Solar Mobility Act creates a general regulatory framework similar to the 1862 Pacific Railroad Act and the 1934 Communications Act:

- The Franchise Ordinance was created to provide people in local areas to obtain Rights of Way access in their cities.

- LMCs should risk very little until the 5X5% Performance Standard is adopted by the local governments:

- Create training and manufacturing localization mechanisms.

- Start small, iterate relentlessly.

- The Kitty Hawk Networks are starter networks designed to train, create local interests, find technology partners, find local investors, and create a community around the shift in infrastructure.

- Capital required of an LMC for a Kitty Hawk Network is:

- $3 million to buy a Kitty Hawk Network (KHN, a fully functional commercial grade network) from JPods LLC.

- $2 million to operate the KHN, pass the Solar Mobility Act, and obtain a Franchise Ordinance for a specific network.

- Construction Capital supports Master Mobility Companies (MMCs) building networks that LMCs have obtained Rights of Way for.

- MMCs use Construction Capital to build networks then sell them to LMCs which operate networks.

- Construction Capital can be from equity, short term bonds (one, two, and three years), and debt.

- Master Mobility Companies will operate with 52 accounting cycles per year.

- Networks completed each week will be sold that week to LMCs to operate.

- These weekly accounting cycles force internal discipline so Nothing Waits™.

- The construction cycle, from survey to sale to LMC, is typically six to nine months long.

- Once manufacturing is fully ramped, an MMC should be able to certify rails at the rate the Transcontinental Railroads were built in the 1860s of 3 to 10 miles of rails per day per crew.

- As networks are certified, Construction Capital will be repaid to the investors or recycled to build more networks depending on the specific agreement with the source of the Construction Capital.

- For the first 100 miles of networks, MMCs will sell networks to LMCs for $30 million per mile.

- Asset Capital is used by LMCs to buy networks from MMCs.

- Asset Capital may be a combination of equity capital, debt, and long term bonds (10-year, 30-year).

- Asset Capital is repaid from fare box earnings.

- There are multiple 10x savings over roads and mass transit that will allow LMCs to repay Asset Capital on-time and agreed to ROI.